Balance Sheet

A balance sheet is a statement, not an account, prepared to show the financial position of a company at a point of time. It is a statement showing the status of capital, liabilities and assets of a company. It is called a Balance Sheet as it balances out the equational relationship of Assets = Capital + Liabilities. A balance sheet is a statement showing what the company owns (Assets) and what the company owes (Capita and Liabilities) on its date of preparation. Balance sheet is correct only if Assets = Capital + Liabilities agrees arithmetically.

The balance sheet consists of two sides: Assetsside and the Capital & Liabilities side. The total of these two sides must be equal to conclude the financial position of the concerned company.

Features of Balance Sheet

- A balance sheet is a statement, not an account

- It prepared for a particular date, no a particular period

- It is prepared after the preparation of the Profit and Loss Account

- The total of two sides of a balance sheet must be equal

- A balance sheet shows the financial position of a company as a going concern

- It helps in the preparation of the Cash Flow Statement

Classification of Assets and Liabilities

We now know that the Balance Sheet is concerned with assets and liabilities. We must know that both assets and liabilities are of different types. The types or classification of assets and liabilities have been discussed below:

Classification of Assets:

- Fixed Assets: These are the assets of a permanent or long-term nature. These are purchased, held and used by the business to generate revenue. These are not for sales during the ordinary course of business. But these can be sold either at the end of their life or at a time when not needed by the business. This includes assets such as buildings, plants and machinery, vehicles etc.

- Current Assets: these are those assets that are acquired by a business either for resale or for conversion into cash. These assets are realized within one year. This includes assets such as cash in hand, cash at bank, debtor, receivable, inventory etc.

- Tangible Assets: These are assets that can be seen, touched and felt. These assets have a certain size or volume. These are mostly of fixed or permanent nature. Assets like building, machinery, motor vehicles etc.

- Intangible Assets: These are assets of a long-term nature that cannot be seen,touched and felt. These do not have physical size or volume. Assets like goodwill, patent, trademark, copyright etc. are included under it.

- Wasting Assets: These are the assets that exhaust or reduce in value due to their use. These are more natural resources whose continuous extraction and use keeps on reducing their quantities. For example, coal mines, petroleum etc.

- Liquid Assets: These are cash or cash equivalent assets that arequickly convertible into cash. These are that part of current assets which have higher liquid status than other current assets. This includes assets like cash in hand, cash at the bank, receivables etc.

- Fictitious Assets: These are not real assets. These are those expenses or losses which are not fully written off. These are large expenses incurred with the expectation of benefit in more than one year in the future. For example, preliminary expenses, advertisement, underwriting commission etc.

Classification of Liabilities:

- Longterm Liabilities: These are liabilities that are not payable during a current accounting year. These are taken for more than one year. Funds raised from such liabilities are used for the purchase of fixed assets by the business. These include liabilities such as a loan on mortgages, bank loans etc.

- Current Liabilities: These are the liabilities that are payable within the current accounting year. Such liabilities occur during the regular course of business operation. These include liabilities such as trade creditor, account payable, bank overdraft etc.

- Owner’s Fund: As per the business entity concept of accounting business and its owner are different. Hence, the business is liable to pay the capital amount brought in by the owner. This is called the owner’s fund. This also adjusts net profit or loss, additional capital, drawing, income tax etc. concerned with the owner.

- Contingent Liabilities: These are those liabilities that are dependent on some situation or condition. Such liabilities happen only when such a condition or situation becomes true. For example, loan guarantee, guarantee for contract etc. Such liabilities are not disclosed in the balance sheet unless they occur or their value is determined. In accounting practice, such liabilities are mentioned as a note below the balance sheet to notify its stakeholders.

Importance of Balance Sheet

A balance sheet is prepared so as to facilitate different aspects. It is important and useful to different users in different ways. Some key importance of the balance sheet has been presented as under:

- Depicts Financial Position: The balance sheet shows the true financial position of a business. It shows the actual assets and liabilities of the business. It is a disclosure statement of the financial picture of the business on its preparation date.

- Calculation of Rate of Returns: Balance sheet provides numerous items and their values to help in the calculation of various rates of returns. Such rates of returns are mostly used by investors. With balance sheet details, different rates of returns such as Return on Equity (ROE), Return on Assets (ROA), Return on Capital Employed (ROCE) etc. can be calculated.

- Risk Assessment: The details of the balance sheet can be used for the risk assessment of a business. The risk associated with the business can be assessed based on capital structure, debt composition, debt repayment status etc. of the business. All the related information can be extracted from the balance sheet.

- Assessment of Liquidity and Solvency: The users of the balance sheet can assess the liquidity and solvency position of the business. Liquidity measures how fast a business can convert current assets into cash and how fast it is paying current liabilities. The solvency position tells about the ability to pay the debt. A high level of debt means low solvency and a low level of debt means high solvency.

- Decision Making: The information available in the balance sheet and its analysis helps in decision-making. Investors, management, debtors, creditors, employees etc. can use the balance sheet and its analysis to make decisions of their concern.

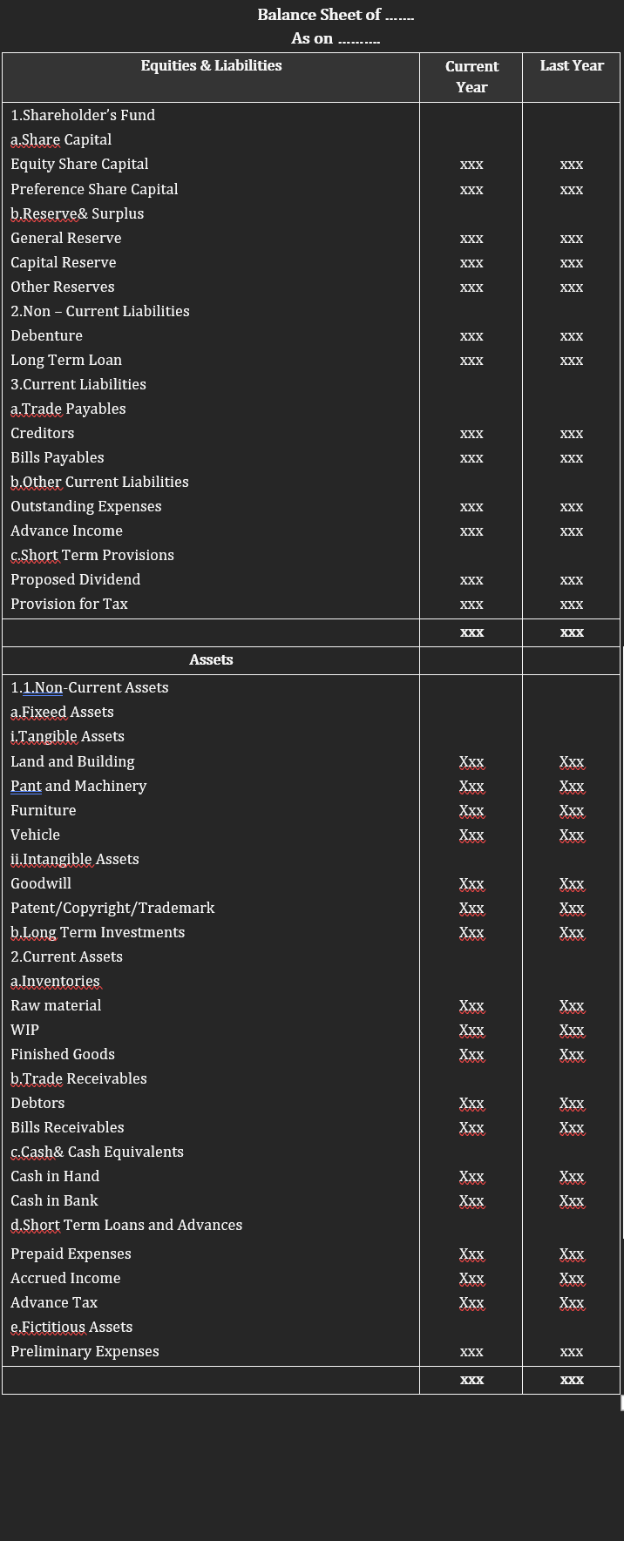

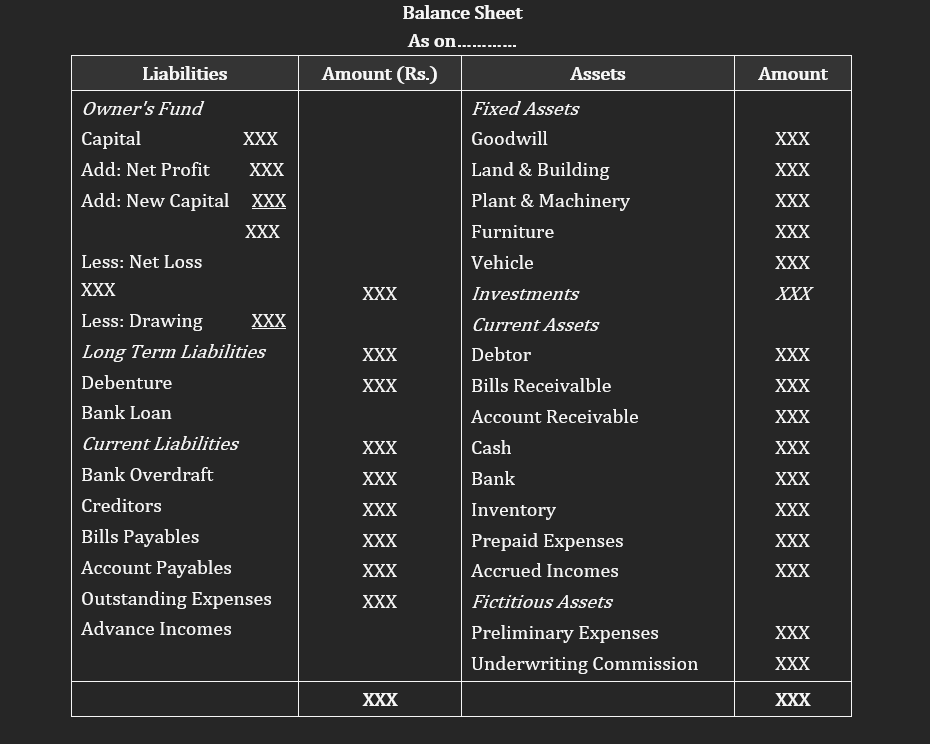

Types of Balance Sheet

Horizontal Balance Sheet

Vertical Balance Sheet