A cash book is a daybook or main entry book used to record all transactions related to cash. It records all cash receipts and all cash payments. A cash book is considered a special day book because of its dual nature in accounting. Cash book acts as the main entry book as well as a ledger in accounting. The dual impact of cash book occurs due to the presence of two sides: ‘Debit’ and ‘Credit’. It is the combination of a cash receipts journal and cash payments journal. That’s why it is also called Cash Receipt and Payment Journal. Receipts and payment vouchers are the source documents for cash book. Receipts are the evidence for cash received and payment vouchers are the evidence for cash payment made.

Since cash is an asset, the recording in a cash book is made under the concept of a real account. This means cash coming in is debited and cash going out is credited in the cash book. This can also be said as an increase in cash is debited and a decrease in cash is credited in the cash book. Any transaction with no cash relevance is not recorded in the cash book.

Types of Cash Book

Depending upon the nature and need of the business, different types of cash books are used. There are mainly four types of cash books. These are explained as under :

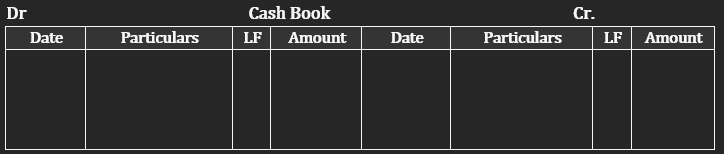

- Simple Cash Book: This type of cash book consists of only one ‘Amount’ column on each side. The cash received is debited and cash paid is credited. This applies to both cash at the office and cash at the bank.

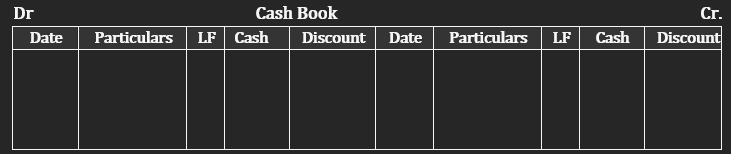

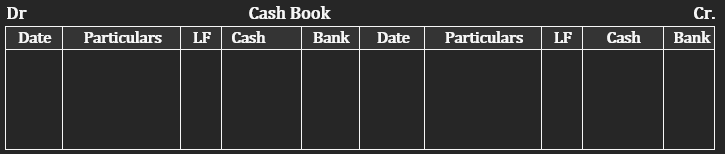

- Double Column Cash Book: This type of cash book consists of two ‘Amount’ columns on both the debit and credit sides. The columns could be in the following orders:

- a.Cash and Discount Column

- b.Cash and Bank Column

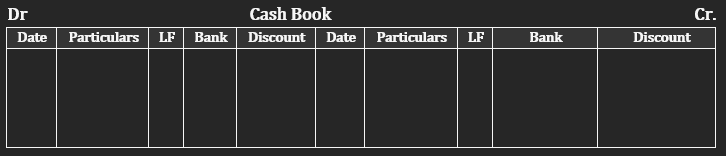

- c.Bank and Discount Column

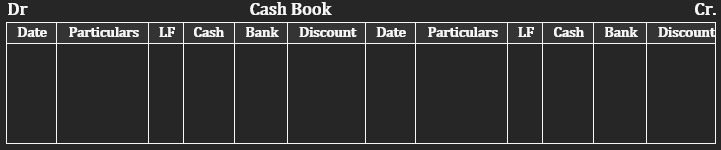

- Triple Column Cash Book: This book consists of three ‘Amount’ columns in each of the debit and credit sides. The three columns are cash at the office, cash at the bank and discount.

- Muti-Column Cash Book: This is the book where receipts and payments are recorded either based on departments (such as sales, production, personnel etc.) or products (such as television, radio, video etc.) or banks (such as NABIL Bank, RastriyaBanijya Bank, Nepal Bank, Agriculture Development Bank etc.).

Specimens:

a.Single Column Cash Book

b. Double Column Cash Book (Cash and Discount Column)

c. Double Column Cash Book (Cash and Bank Column)

d. Double Column Cash Book (Bank and Discount Column)

e. Triple Column Cash Book