Meaning of Cash Flow Statement

Financial statements like Profit and Loss Account, Balance Sheet and Shareholder’s Equity Account cannot answer the questions regarding the cash of a company. A company in operation generates cash from different sources and uses it for different activities. Such details of sources and uses of cash in an organization are provided by a cash flow statement. It provides cash inflow and outflow of a firm during an accounting year. Hence, it can be regarded as a statement showing changes in cash position due to changes in balance sheet position from the previous year to the current year.

A cashflow statement is the statement of cash flow during the business. Cashflows are inflows and outflows of cash and cash equivalents. That’s why, cash flow statement is the overall report of cash coming, going out and change in the business. It is a report of cash flow from operating activity, investing activity, financing activity and net change in cash position thereof.

Objectives of Cash Flow Statement

- To provide information about cash receipts and a cash payment of an organization during an accounting period

- To provide information about an organization’s operating, investing and financing activities during the accounting period

- To show the status of change in the cash position of the organization

- To evaluate the financial policies of the organization

- To help in the understanding liquidity position of the organization

- To find out reasons causing variation in cash position

- To support the short term cash planning of the organization

Importance of Cash Flow Statement

The importance and usefulness of the cash flow statement have increased significantly. It is regarded as a key part of the financial statement of any organization. Hence, international and national laws have made it mandatory to be published with other financial statements. In this context, the importance of cash flow statement has been presented below:

- The true cash position of an organization can easily be identified as a cash flow statement that deals only with cash

- It helps in planning and co-ordinating financial operation properly in an organization

- It assists in strengthening the internal financial position of an organization

- It supports long-term cash planning such as repayment of a loan, replacement of assets etc.

- It helps in identifying changes in the position of debtor, inventory, creditor etc. and depending upon theirfavourability, different relevant policies can be formulated

- It is important for investment decision, tax liability and competitors’ analysis of an organization

- It reflects liquidity and solvency position at a glance

Steps in Preparation of Cash Flow Statement

Cash flow statements should report cash flow during the period classified by operating, investing and financing activities. Based on the mentioned categories, the following steps are to be performed at the time of preparing the cash flow statement:

Step 1:

Determination of Cash Flow From Operating Activities (CFOA)

Those transactions which are taken into account at the time of calculating net profit are called operating activities. These are the key revenue-generating activities of the business which are not related to investing or financing activities. That’s why it can be said that cash other than investing and financing activities are cash flow from operating activities. According to NAS, the following are the examples of cash flow from operating activities:

- Cash received from the sales of goods and the rendering of services

- Cash received from royalties, fees, commission and other revenue

- Cash payment to suppliers for goods and services

- Cash payment to and on behalf of employees

- Cash received and payment of an insurance enterprises for premium and claims, annuities and other policy benefits

- Cash payment or refund of income tax unless they can be specifically identified with financing and investing activities

- Cash receipts and payments from contracts held for dealing or trading process

Based on the above examples, the calculation of cash flow from operating activities can be divided into four categories. These are stated as under:

- Cash received from customers

- Cash payment for the purchase of merchandise

- Cash payment for expenses

- Cash received from interest and dividend

Step 2:

Determination of Cash Flow From Investing Activities (CFIA)

Investing activities are related to long-term assets. In other words, investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents. Hence, cash concerning such activities is regarded as cash flow from investing activities. According to NAS, the following are the examples of cash flow from investing activities:

- Cash payment to acquire property, plant and equipment, intangibles and other long term assets

- Cash payment to acquire equity or debt instrument of other enterprises

- Advance cash and loans given to other parties

- Cash payments made for further contract, forward contract, option contract and swap contract

- Cash received from sales of property

- Cash received from sales of equities and debt instruments of other enterprises

- Cash received from the repayment of advance and loan given to other parties

- Cash received from further contracts

Step 3:

Determination of Cash Flow From Financing Activities (CFFA)

Shareholders’ equity and long-term liabilities are considered under financing activities. Financing activities are those activities concerned with changing the size and composition of equities and long-term borrowing. Hence, cash flow from financing activities is those resulting from financing activities of the enterprise. Some examples of cash flow arising from financing activities are mentioned below:

- Cash proceeds from the issue of a share, debenture, loan, notes, bonds and mortgages and another short or long term borrowing

- Cash paid to owners to redeem the share, repayment of borrowing and for the reduction of outstanding liability related to a finance lease

- Payment of dividend

Step 4:

Finding Net Change in Cash and Closing Cash Flow Statement

After determining cash flow from operating, investing and financing activities, the obtained cash flows are added. The result of the addition is the net change in cash flow from last year to the current year. The change could be either an increase or decrease in cash flow. In this net change, the cash and cash equivalents of last year are added. The result from the addition is the closing cash and cash equivalents for the current year. After this, the cash flow statement is closed.

Methods of Cash Flow Statement

There are two methods of preparing a cash flow statement. These are explained as under:

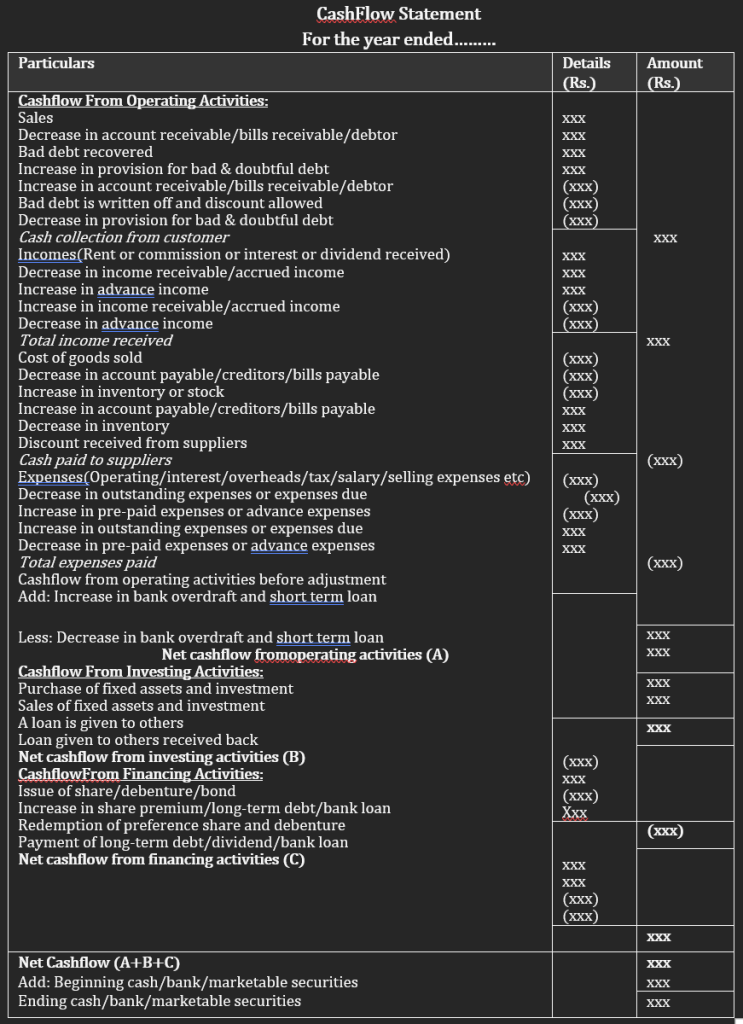

1. Direct Method: This is one of the most used methods of preparing a cash flow statement. Under this cash flow from operating, investing and financing activities are determined and adjusted with opening cash and cash equivalents. With this,the ending cash and cash equivalents are determined. Following is the technique of preparing a cash flow statement under this method:

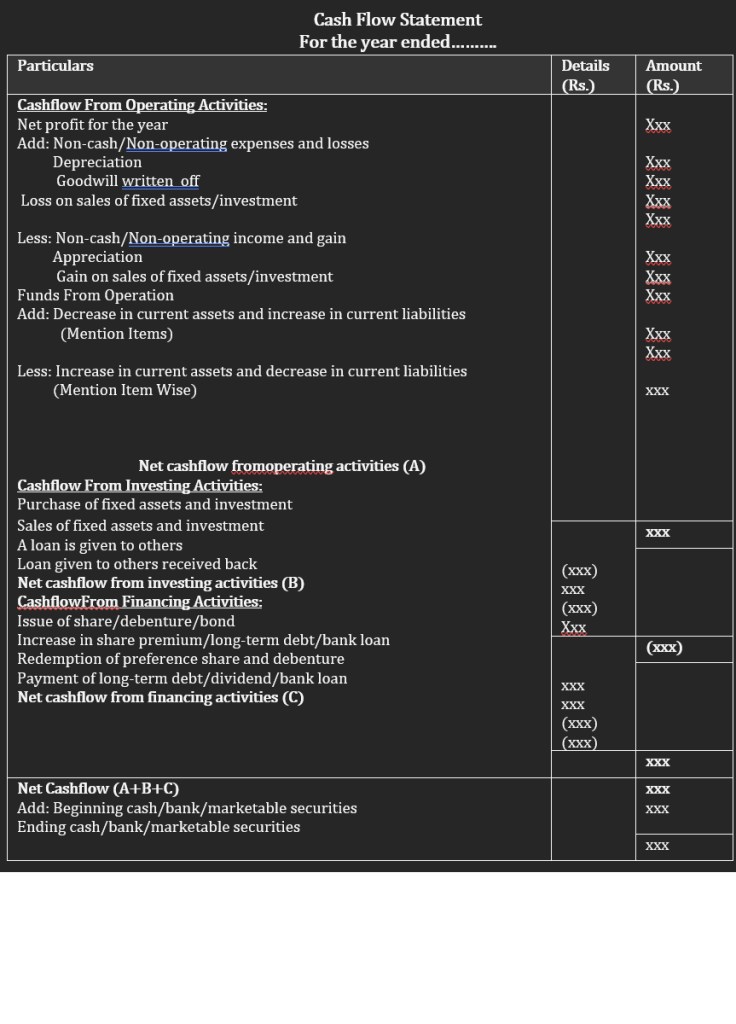

2. Indirect Method: This is a method with a slight difference from than direct method. Under this method, all the calculations are the same as the indirect method except the computation of cash flow from operating activities. For cash flow from operating activities, this method uses adjustment with the help of net profit for the year. The cash flow statement under this method is prepared as below: