Concept of P/L Account

Profit and Loss Account is a financial statement prepared after the preparation of the Trading Account. SO, this can be regarded as the second step in the preparation of a financial statement. The profit and loss account is prepared by adding all the indirect incomes to Gross Profit or Gross Loss resulted in the trading account and subtracting all the indirect expenses of the business. The resulting value from doing so is either Net Profit or Net Loss. In other words, it is an account prepared to obtain profit or loss of a business after considering all indirect expenses and indirect incomes.

The preparation of profit and loss accounts follows the accrual system of accounting. This means all the expenses and incomes at they occurred are taken into consideration. This is prepared on yearly basis matching all the expenses and incomes to get the resulting net profit or net loss. Noticeably, all the indirect and abnormal losses, as well as gains, are also considered while preparing profit and loss accounts.

Purpose of P/L Account

- To ascertain profitability position of business through the determination of net profit or net loss, mostly on a yearly basis

- To initiate steps for effective control of expenses which are on the higher side

- To facilitate the preparation of other financial statements such as Balance Sheet and Cash Flow Statement

- To help in financial analysis of the business by providing different variables their values

Contents of P/L Account

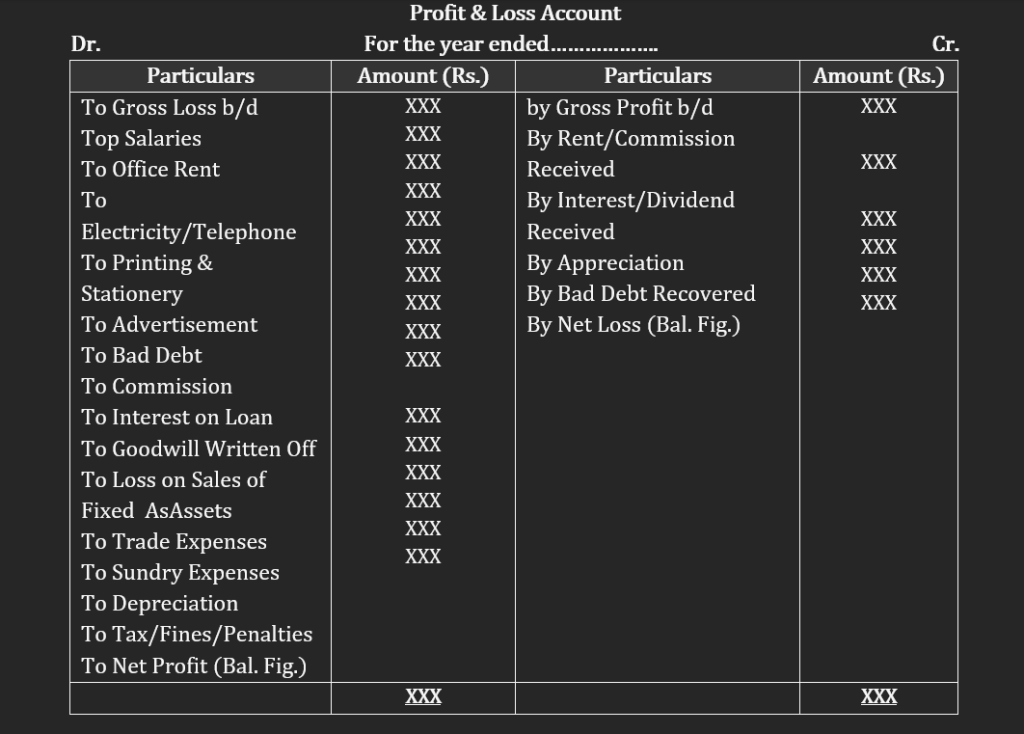

Basically, the profit and loss account deals with indirect expenses and indirect incomes to determine net profit or loss. Moreover, it deals with other contents or items too. The contents or items of the profit and loss account has been mentioned below:

Contents of Debit Side

- Gross loss carried forwarded from Trading Account

- Office and Administrative Expenses such as office rent, salaries to staff, electricity bills, postage and telegrams, telephone, printing and stationery, audit fees, legal charges, repair and renewals etc.

- Selling and Distribution Expenses such as advertisement, carriage on sales, sales commission, godown expenses freight on sales, sample expenses, insurance related to goods, bad debt etc.

- Financial Charges such as interest on a loan, loan renewal fees, a dividend paid etc.

- Abnormal Losses such as loss on sales of fixed assets or investment, goods lost by fire (not insured), loss due to theft etc.

- Written Offs related to intangible assets like goodwill, patents, copyright etc. and long-term expenses such as preliminary expenses, long-term advertisements etc.

- Expenses Payable to Government such as tax, fines and penalties

- Depreciation of fixed assets

- Net Profit (balancing figure of the account)

Contents of Credit Side:

- Gross Profit carried forward from Trading Account

- Indirect Incomes such as commission received, rent received interest on investment etc.

- Abnormal Gains such as gain on sales of fixed assets or investment, bad debt recovered etc.

- Appreciation of fixed assets

- Net Loss (balancing figure of the account)

Profit and Loss Account (Sample)